User Power

Value/Post Ratio

418%

- Feb 15, 2019

- 242

- 1,012

- 25

To all my fellow real estate people, I thought you may benefit from this tactic I'm using to get crazy low interest rate debt.

We like to call it Borrowing money the long way, here's how it works (the numbers are from a real deal I'm currently doing):

Seller has a house listed for 165k

I offer them 15k down, and they carry 150k, 500/mo for 300 months 0% interest. The key, I say I want to attach this debt to a different property, not the subject property I'm buying.

Seller accepts my offer

The house is realistically probably worth 140k.

After closing on the property, I turn around and list the house on the market for 140k.

Get an offer for 140k and sell the house.

I pay 6% realtor commissions and 1,600 or so in closing costs

Leaving me with 130k.

I gave the seller 15k down, so I'm really getting out 115k that is "new money" so to speak.

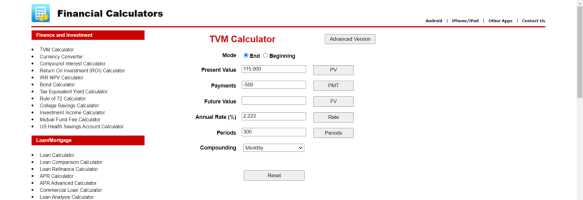

With the seller financed debt being attached to another property I'm able to walk out of the closing with 115k cash that I can go do whatever I would like with. I'm paying 500/mo for 300 months to have 115k. That imputes a 2.22% interest rate when plugged into a financial calculator. Will attach a screenshot to show calculation.

The best part, I now have a 25k loss that I'm writing off my tax bill. I paid 165k for the house, only sold it for 140k.

If you don't have free and clear property to attach the mortgage to you can get a hard money loan against the house you're buying, pay off another property and attach the mortgage to your other property you just paid off with the hard money loan. Once you sell the subject house, the hard money loan will pay off and you likely won't walk out of there with any cash. But you did just refinance your other property at a 2.22% rate. Of course, these are non-recourse loans with no personal guarantee as they are seller financed.

I've got 4 of these deals currently going as I continue to refinance out some of my higher interest debts on properties/use it to buy new deals. Cool tactic, and some of the best debt you'll ever find.

We like to call it Borrowing money the long way, here's how it works (the numbers are from a real deal I'm currently doing):

Seller has a house listed for 165k

I offer them 15k down, and they carry 150k, 500/mo for 300 months 0% interest. The key, I say I want to attach this debt to a different property, not the subject property I'm buying.

Seller accepts my offer

The house is realistically probably worth 140k.

After closing on the property, I turn around and list the house on the market for 140k.

Get an offer for 140k and sell the house.

I pay 6% realtor commissions and 1,600 or so in closing costs

Leaving me with 130k.

I gave the seller 15k down, so I'm really getting out 115k that is "new money" so to speak.

With the seller financed debt being attached to another property I'm able to walk out of the closing with 115k cash that I can go do whatever I would like with. I'm paying 500/mo for 300 months to have 115k. That imputes a 2.22% interest rate when plugged into a financial calculator. Will attach a screenshot to show calculation.

The best part, I now have a 25k loss that I'm writing off my tax bill. I paid 165k for the house, only sold it for 140k.

If you don't have free and clear property to attach the mortgage to you can get a hard money loan against the house you're buying, pay off another property and attach the mortgage to your other property you just paid off with the hard money loan. Once you sell the subject house, the hard money loan will pay off and you likely won't walk out of there with any cash. But you did just refinance your other property at a 2.22% rate. Of course, these are non-recourse loans with no personal guarantee as they are seller financed.

I've got 4 of these deals currently going as I continue to refinance out some of my higher interest debts on properties/use it to buy new deals. Cool tactic, and some of the best debt you'll ever find.

Dislike ads? Remove them and support the forum:

Subscribe to Fastlane Insiders.

Attachments

Last edited:

") But I give mad props to people like Casey and you for coming up with these, they are brain twisters and best of all, they do get some deals done!

But I give mad props to people like Casey and you for coming up with these, they are brain twisters and best of all, they do get some deals done!

") . Keep up the good work!

. Keep up the good work!